Why Market Structure Matters

The Importance of Market Structure Related Services

July 12, 2017

By:

Richard Johnson

Table of Contents

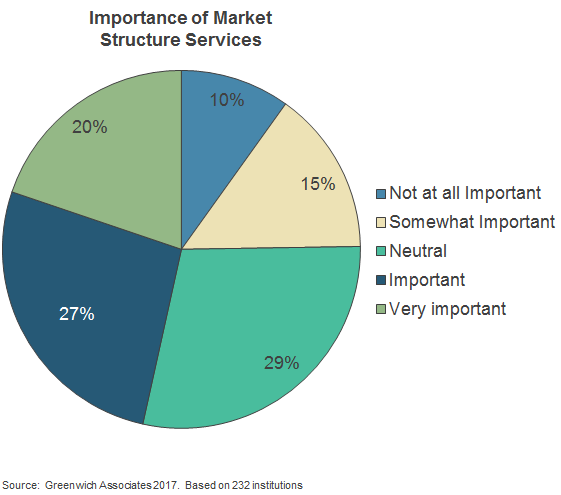

Investors continue to thirst for market structure information. In our most recent U.S. equities study, almost half of buy-side respondents told us that sell-side provision of market-structure-related services was either important or very important. This sentiment was even more pronounced among larger accounts and institutional managers. And while broker-dealers continue to have a tough time equating investments in market structure with increases in market share, clients clearly believe this correlation exists.

Advice Highly Valued

It should come as no surprise then that every large broker now offers market structure advice and related services to their clients. For some, it is an ancillary service provided by the desk, while at others, it is a key differentiator with a dedicated team. So why has a subject that bridges the technical minutiae of market mechanics and the legalese of government regulations come to be so valued?

As our markets have become increasingly complex, even the smallest change to market structure can cause a significant impact on trading performance—like a high-performance sailboat, a slight variation in route or rigging configuration can have a meaningful impact on competitiveness.

Brokers and venues are continually innovating, developing new matching systems, algos and order types that they hope will drive increased business. At the same time, the nature of liquidity itself is constantly changing, as new players enter the market and market conditions change the types of strategy that are used. Market structure is never static—it is constantly moving and shifting like Brownian motion. For traders, staying on top of market structure issues can give them an advantage, as they seek to optimize their trading strategy and improve performance.

Regulatory Changes Shape Corporate Strategy

As we have seen, regulatory changes can have a huge impact on how our markets function. Regulations such as Reg ATS, decimalization and Reg NMS all had a profound effect on the competitive dynamics of trading, reducing the profitability of some business models and creating opportunities for others. For many companies, staying on top of market structure is a vital part of corporate strategy. Reg NMS may, in fact, have been the catalyst for the emergence of market structure as a competency. As traders dealt with fragmentation, HFT and other downstream consequences, they realized that market structure was too important to be left to lawyers and regulators and that their voice needed to be heard too.

Today the level of debate we are having on these important topics is a far cry from just 10 years ago. In addition to the experts on both the buy and sell side—not to mention independent companies like Greenwich Associates—there are now numerous conferences and working groups discussing these important topics. And of course, there is the Equity Market Structure Advisory Committee whose quarterly meetings are now live streamed across Wall Street.

When asset managers, brokers, exchanges and other market participants have an informed opinion on the issues and a voice in the debate, the outcome will be better markets for all investors and traders.