Recognizing Standout Equity Trading Brokers Amid Market Turmoil

Table of Contents

As COVID-19 plunged equity markets into turmoil in mid-March, volatility and trading volume exploded.

At the same time, the health crisis forced brokers abruptly away from their trading floors, threatening to disrupt their ability to maintain well-functioning operations and service their clients—who were also working remotely—when they were needed most for insights and execution.

Looking back weeks later, the buy side and sell side both adapted well during this unprecedented stress test. Following a short period of adjustment, most brokers mobilized to deliver robust front-office coverage that met their clients’ needs.

By mid-April, when we reached out to North American buy-side traders regarding their experiences during those first weeks of the crisis, a remarkable 80% were satisfied with brokers’ performances in providing liquidity, hedging solutions, market color, and insights, including nearly 50% who were highly satisfied, despite some issues raised about settlement processes.

Standout Brokers

As part of those conversations, we also asked buy-side traders to name the brokers whose execution coverage had been most helpful to them in navigating the market turmoil caused by COVID-19. The following six firms garnered the most mentions and were closely grouped:

Outside of the bulge bracket firms, Instinet, JonesTrading, RBC Capital Markets, and Virtu also stood out for their execution support among clients.

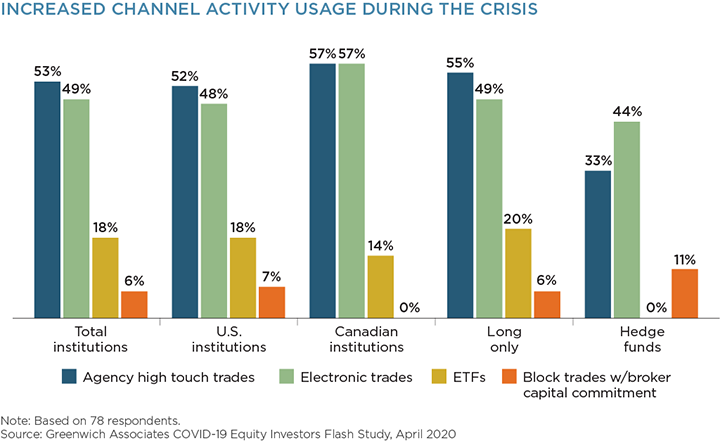

Since the outbreak, just over half of institutions shifted their equity volume mix toward more agency high-touch trades, while a nearly equal proportion significantly increased the use of electronic trading. Brokers that received the most citations in this flash study were well positioned to meet investors’ changing needs in this unusual environment, as evidenced by their strong capabilities and broad relationships in our equities studies in recent years.

Unique Challenges in a Competitive Business

It should be noted that more than 50 brokers in total were named by investors as having been particularly helpful during the turbulent weeks in March and early April. The sheer number reflects the fiercely competitive nature of the equities business and is a reminder that gains can be transient and firms that have performed well in the short term will need to continually invest and adapt to maintain their edge.

The unique challenges posed by COVID-19 will also prompt sell-side management to ponder the optimal client coverage model during and post-crisis, e.g., local vs. remote, specialist vs. generalist, and mix of senior vs. junior staff.

One outcome is not in doubt: The crisis has underscored the need for all firms large and small to continue to invest in technology, both in execution and in workflow.

Navigating Turbulent Market Series

Partnering with Clients in a Time of Market Turmoil

COVID-19 Impact on FICC Markets

COVID-19 Impact on Equity Markets