Tapping the Network Effect to Unearth Bond Liquidity

Table of Contents

Competition among fixed-income trading platforms is increasingly fierce. Despite an already impressive run-up in electronic trading levels, expectations for growth in this segment are so high that an arms race is underway among those trying to take part.

The ways in which they compete, however, has changed. When most of these platforms were originally founded—some 20 years ago and some less than five—the biggest challenge was to convince liquidity providers to become active on the venue, which in turn attracted the buy side to come in search of liquidity.

This was, and still is, no small feat that remains a notable chicken or egg problem. Liquidity providers go where their customers might be, and the customers only go where they see liquidity. As we’ve written in the past, trading venues, like social media platforms, are no fun if you’re the only one there.

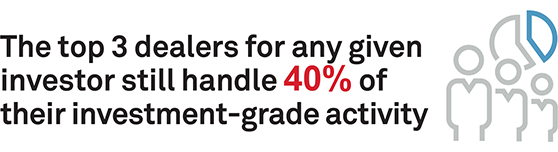

Today, however, differentiating based solely on liquidity providers on the platform doesn’t cut it anymore. Don’t get me wrong, the size of the network matters—especially as the number of market participants able to provide liquidity has expanded to include all manner of buy- and sell-side firms. However, Coalition Greenwich data shows that the top 3 dealers for any given investor still handle 40% of their investment grade activity.

Moreover, at minimum, the top 20 dealers by volume are on all of the main corporate bond platforms. So, having liquidity providers on the platform in and of itself isn’t enough to get the buy side excited about something new—it is now just table stakes.

Price Improvement is Key

Trading venues increasingly stand out based on their ability to provide price improvement, which today comes from access to unique liquidity. Unique liquidity can sometimes come from unique liquidity providers—perhaps an emerging nonbank liquidity provider or regional bank.

But increasingly, unique liquidity involves unearthing buy and sell interest regardless of firm type. Asset managers, hedge funds and even pension funds can enter the equation when platforms provide more seamless methods to connect everyone with everyone.

The dealers should not be left out of this conversation, however. While big-dealer dominance used to come from their large balance sheets, which allowed them to take principal risk, their dominance now is based much more on the network of clients they’ve created over time, and their ability to connect opposing interests among them. In other words, they know where the bonds are buried.

You might be thinking “that’s always been the case”—and you'd be correct. However, today there are so many more bonds and so many market participants that trading in this space without the right technology is nearly impossible. Each major bank effectively has its own ecosystem of customers and partners, similar to the networks created by the largest trading venues.

A lot of work has been done over the past decade using artificial intelligence and (perhaps less novel) database technologies to pour through every manner of customer interaction in those ecosystems—be it chat messages, phone calls, expressed interest in a bond—to provide the sell-side trader with ideas on whom to call about which bonds.

The Quest for Smart Transparency

Nevertheless, there is still room for improvement in both the technology and the process. First, there is a continued push to increase market transparency without creating information leakage. Put another way, how can corporate bond investors express interest in a bond and understand current market pricing and depth without showing their hand? The goal is to create “smart transparency” that optimizes price discovery while minimizing information leakage.

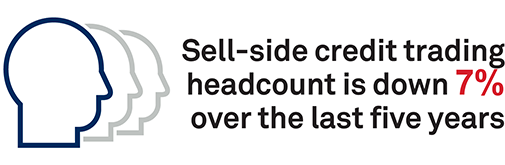

Second, with sell-side credit trading headcount down 7% over the last five years according to Coalition Greenwich data, bond dealers need to more effectively mine their long-curated network of bond buyers and sellers to find the right matches at the right time. This should mean not only finding one buyer to match every seller’s interest, but perhaps finding enough buyers to match a single seller’s interest.

To that point, there is an opportunity to expand upon the current market model of matching one buyer to one seller by allowing multiple buyers to more easily fill the order of a single seller. Mechanisms to achieve this today are limited, in part because of the long-held market convention and, in part, because of a fear of information leakage.

The RFQ winner’s curse could be made worse if the market knew only a portion of the order was filled, leaving the rest to trade (or not) at another price with another liquidity provider. Solving this challenge could continue the string of wins for innovative trading venues that have unlocked liquidity that would not have been found a decade ago, while allowing the buy side to still tap the sell side’s deep trading networks.

Improving Best-Ex Analysis

Over the last decade, fixed-income electronic-trading growth has also taught us that allowing dealers to continue to do what they do best—provide liquidity via their balance sheet or via their distribution network—must remain a part of the new market structure. While technology has changed how the dealers do what they do, it doesn’t change what they do. As such, enhancing those capabilities is a more likely path to success than trying to diminish or move them elsewhere.

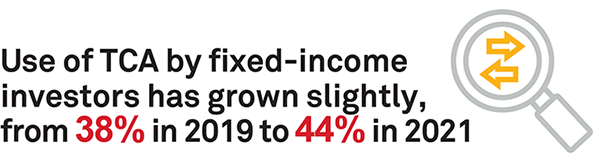

To move forward with these and other ideas, best-execution analysis must become more science than art so that traders can measure price improvement across platforms and dealers more effectively. Use of transaction cost analysis (TCA) by fixed-income investors has grown slightly, from 38% in 2019 to 44% in 2021, according to Coalition Greenwich data. But in most cases, the analytics are used post-trade and provide only limited insight into the liquidity-seeking process at the time of trade.

Furthermore, as corporate bond trading has become more systematic over the past decade, so too should dealer and venue selection. Such analyses must be backed by solid data and models that have been proven over time. Otherwise, comparing best-ex reports is doomed to remain in the realm of arguing over how many angels can dance on the head of a pin.

Ideas that look great on paper only become truly great when they help market participants make (or save) money. When refined through the fierce forges of intense competition, the best systems prove out that they can deliver that most sought-after of outputs—price-improved executions from unique liquidity.